At the most recent CDS Advisory Board meeting, some of Scotland’s key industry figures gathered to discuss how ‘stakeholder banks’ can be the ideal solution for co-operatives looking to raise capital.

At the most recent CDS Advisory Board meeting, some of Scotland’s key industry figures gathered to discuss how ‘stakeholder banks’ can be the ideal solution for co-operatives looking to raise capital.

Jaye Martin, a Specialist Advisor at CDS, shares her experience of the day.

As January comes rapidly to an end and the weather shows no signs of improvement, like me, you are probably longing to get away from the soggy grey skies.

But at the recent CDS Advisory Board session, we refused to be cowed by the January blues and instead presenting an eclectic mix of speakers to throw some light (and shade) on the topic of Financing and Capitalising Co-operatives.

James Graham of SAOS

Insights gained from the session will help inform our thinking over the coming year as we consider in sharper detail the financing issues affecting the businesses we work with particularly relating to employee buyouts and consortia of scale. This is of course in the wider context of Scottish Enterprise’s ongoing work in the Access to Finance arena and the Scottish Government’s Sustainable, Responsible Banking strategy, published last year.

Attendees from CDS, our Advisory Board, Scottish Enterprise and the Scottish Government heard from James Graham of SAOS on the challenges of capitalising a typical agricultural co-op and the potential need for a farming and rural financial intermediary to serve that community, and Angus Waugh and Gerry Sweeney from First Milk on the challenges of raising capital in a 1,700 member strong dairy co-operative.

New Economics Foundation’s Tony Greenham gave an in-depth analysis of the UK’s banking system and the benefits of ‘stakeholder banks’ with Rod Ashley of Airdrie Savings Bank, the UK’s last remaining independent savings bank, highlighting the benefits of local banking.

Trying to summarise the rich learning and discussion from this jam-packed session is probably an injustice. However, as a taster let’s consider on the top five financing facts:

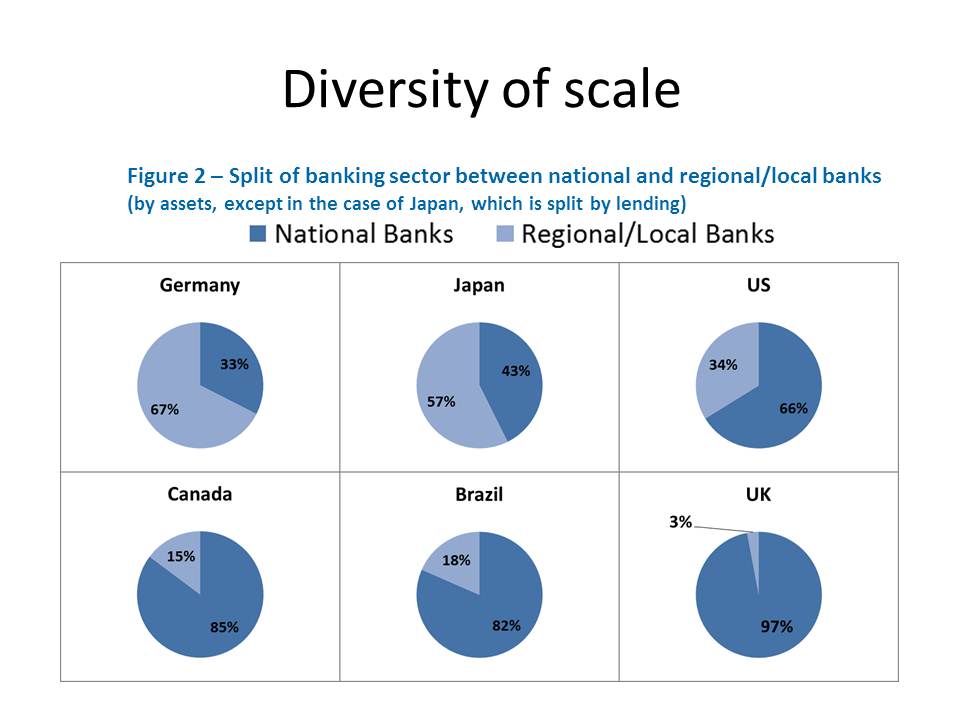

- The UK, and particularly Scotland, lacks diversity in its banking system as compared to other developed nations. In the UK, local banks comprise just 3% of the sector as compared to 67% in Germany and 34% in the USA.

- Co-operative (and employee-owned) business models by their very nature make capital-raising difficult due to the ownership structure. In the USA, there are special provisions supported as a necessary counterbalance to other types of enterprise.

- Collaboration is the name of the game in Germany. Local banks co-own central services (for example, back office, regulatory and marketing functions). This collaboration (rather than the consolidation seen in the UK) allows them to remain locally focused, with sophisticated systems.

Rod Ashley, chief executive of Airdrie Savings Bank.

- Airdrie Savings Bank was founded on 1 January 1835 and is the only institution now operating under the auspices of the Savings Bank (Scotland) Act 1819. Customers have ready access to bank managers and staff with knowledge of the local area and local businesses. The Bank faces an ever increasing scrutiny from the regulatory landscape.

- There are comparatively higher levels of lending to co-ops, social enterprises and charities as well as local SMEs by local banks. For example, the German government-owned development bank KfW has specific funding available for family businesses to help the younger generation to buy out the older (retiring) generation.

Although, like the January sun, this is just a brief account of the topics, the discussion will help us to put finance in the hot seat in 2014.

CDS is here to help businesses considering the adoption of co-operative business models.